The Economy, the Fed, and Rates

July 29, 2025

The Economy, the Fed, and Rates…

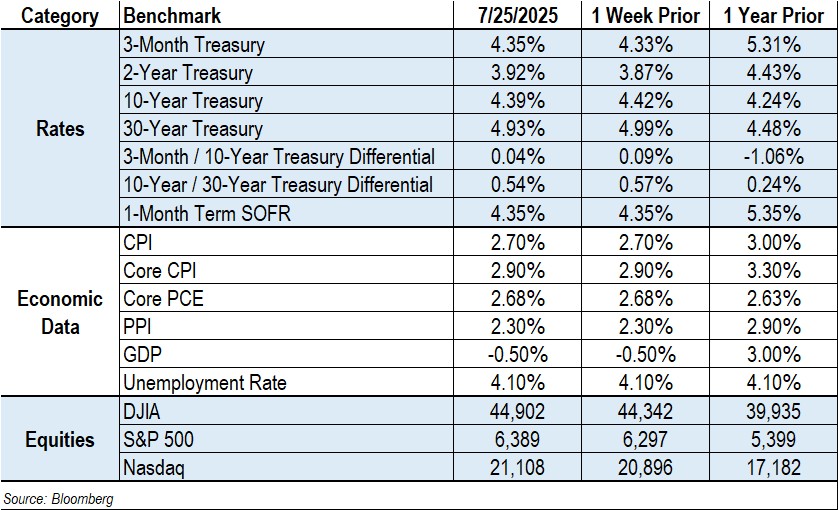

- GDP Outlook Surprises to the Upside: Despite aggressive tariff policies and restrictive immigration measures under President Trump’s second term, the U.S. economy has remained resilient. After a Q1 GDP contraction of 0.5%, widely attributed to pre-tariff inventory stockpiling, Q2 growth is projected at 2.4% according to the Atlanta Fed’s GDPNow forecast. This defied expectations of a slowdown.

- Durable Goods Weakness: U.S. durable goods orders plunged 9.3% in June, reversing a strong May gain driven by aircraft orders. Excluding transportation, orders rose only 0.2%, suggesting business investment is weakening.

- Housing Market Slump: The housing sector has slumped under the weight of high prices and high mortgage rates. Sales of existing homes dropped to a nine-month low in June, indicating that tight monetary conditions and affordability challenges continue to constrain the market.

Federal Reserve Policy

- Status Quo at July FOMC, But September Cut Likely: The Fed is expected to hold rates at 4.25%-4.50% at its July 30 meeting, despite heavy political pressure from President Trump for immediate cuts. Fed funds futures assign ~60% probability of a 25-bp cut in September, with markets pricing in a second cut by year-end.

- Internal Division Emerging: Two Trump-appointed governors, Christopher Waller and Michelle Bowman, may dissent in favor of an immediate cut. A double dissent by governors would mark the first such event since 1993 and could indicate a meaningful policy shift ahead.

- Fed Communication under Scrutiny: Former Chair Bernanke recommends greater transparency and use of a “central forecast,” but risks include confusing markets and exposing the Fed to more political attack in a uniquely toxic environment.

- Powell under Pressure: Political attacks on Fed Chair Jerome Powell have intensified, including the president’s questioning whether he should fire him. Though Powell’s term runs through May 2026, speculation about his potential ouster has unsettled markets. PIMCO warned that any move undermining Fed independence would be “very bad for markets.”

Market Reaction and Forward Outlook

- Treasury Yields Easing after Prior Surge: The 10-year Treasury yield fell 3 bps to 4.39% this week, snapping a three-week streak of increases. The decline came amid a flurry of economic data and developments in the ongoing trade negotiations. However, yields remain elevated, reflecting lingering concerns about inflation risks and skepticism regarding fiscal discipline.

- Equities and Corporate Earnings: U.S. equities have rebounded after an early-year dip, supported by strong Q2 earnings – 80% of S&P 500 companies reporting so far have beaten estimates. Another reason for the rebound is that employers continue to hire at a solid clip, and businesses aren't firing people, keeping the unemployment rate at a historically low rate of 4.1%. This resilience comes even as concerns mount about tariffs and Fed policy.

- Tariff Impact Still to Come: While the immediate inflationary effects of tariffs have been muted, analysts caution that cost pass-throughs by businesses could accelerate if tariffs remain in place through year-end. Goldman Sachs cut its 2025 GDP forecast to 1.1%, citing policy uncertainty and structural drags from immigration curbs.

Implications for CRE Finance

- Financing Costs: Even after this week’s rally, mid-4% Treasuries still translate to mid-6% all-in coupons, keeping refinancing math challenging.

- Cap-Ex Pause: The 0.7% slide in core orders and tariff uncertainty suggest that tenants may defer equipment and warehouse expansions – headwinds for industrial absorption.

- Underwriting Discipline: With policy uncertainty and potential Fed dissent, lenders are likely to maintain conservative LTVs and DSCRs, and favor fixed-rate or well-hedged structures.

You can download CREFC’s one-page MarketMetrics, which includes statistics covering the economy and the CRE debt capital markets,

here.

Contact

Raj Aidasani (

raidasani@crefc.org) with any questions.